Narrowing the retirement savings gap

Tips to consider to help women avoid a potential shortfall in retirement savings.

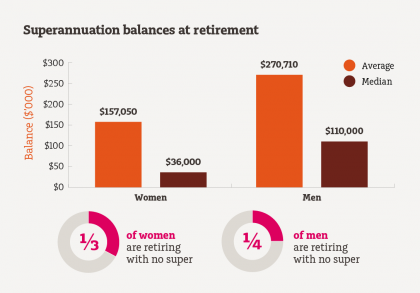

The financial wellbeing of women in retirement is a significant and growing concern, as women still lag substantially when it comes to retirement balances. On average, a woman retires with $157,050, while a man’s average balance is 72% more, at $270,7101. So why is this? And what can women do now to change their outcome in retirement?

Source - bar and pie charts: ‘Superannuation account balances by age and gender’, Association of Superannuation Funds of Australia, October 2017.

It’s not just the gender pay gap

While most people immediately point to the gender pay gap, there’s a need to look deeper. Research shows that many women put the needs of others before their own: a lot of women are primary carers for children2 and, in 70% of cases, women are the primary carers for aging parents3. Inevitably this means more women are working part time – currently 46% of working women do – and this impacts their retirement savings pool4. Often the woman’s long-term financial wellbeing is not considered when the decision to work part-time is made.

Retirement literacy is also an important issue to consider. A recent study in the US found women have lower retirement literacy rates than men5. In Australia, a government report found women are generally highly confident in their ability with money, especially when it comes to budgeting, saving, dealing with credit and managing debt, however they’re less confident than men when it comes to more complex issues like investing, understanding financial language and ensuring enough money for retirement6. More education is needed to support people in their planning.

And, once they’re in retirement, women tend to live longer than men7. This means their money needs to last longer. Cognitive research shows that women tend to invest more conservatively than men8. While investing conservatively is beneficial in preserving retirement savings, it can have an impact on funds that need to grow to help meet the increasing costs of a retirement lifestyle.

Case study: the impact of taking time out

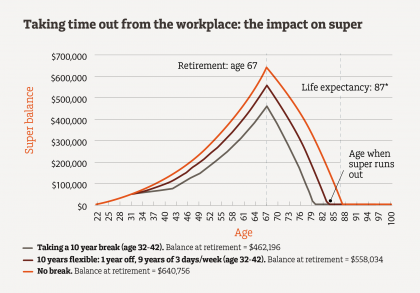

When women decide to take time-off or work part-time, the conversation is usually about the impact this will have on the household budget. Rarely do women look at the impact this will have on their superannuation balances.

To help illustrate the impact, let’s look at three different scenarios a woman may face in her working life: 1. taking a 10 year break from the workplace to look after children full time; 2. Working flexibly for 10 years, for the equivalent of 3 days a week; 3. Not taking any time-out.

The chart below compares her super account balance at retirement and the age at which her retirement savings will run out.

Source: NAB Asset Management Services Limited. For illustrative purposes only. Amounts are shown in today’s dollars: the person starts working at age 22 and retires at 67. Initial salary $50,000 pa, 1% salary increase pa. Salary increases during the time off work. 9.5% pa of salary contributed to super. Retirement income is $47,000 pa. The assumed fund average return is 4.5% pa. When on leave for 10 years, no super is contributed. When working flexibly, salary is calculated at 60%, during ages 32-42. No Age Pension received. Insurance premiums haven't been taken into account, super taxes have. Other investments are not taken into account. Do not rely on this chart to make decisions about your retirement.*The life expectancy of a 67 year old woman today is 87 years. Source: Based on Australian Bureau of Statistics data, Life Tables, States, Territories and Australia, 2014-2016. Catalogue no. 3302.0.55.001.

Lower or no super contributions over the ten year period means there’s less capital to grow, which has a huge impact on two of the super balances at retirement, which will then run out faster in retirement (unless spending reduces).

Today, many companies offer paid parental leave, on top of any government payments. Some businesses also continue to contribute to super during periods of parental leave, which can have a big impact on your balance over the longer-term. These types of incentives are important to consider when assessing potential employers.

Single women have more to consider

While the factors discussed result in sub-optimal retirement outcomes for women generally, the area of greatest concern is for single women – just one in four can expect to have enough super to reach ASFA’s ‘Comfortable’ standard for retirement income, $545,0009. What’s more, the superannuation component of retirement income for single females is 32% lower than for single males10.

Much of this can come down to working part time or taking time out of the workforce. But increasingly we’re also seeing the financial impact that a separation or divorce can have on women.

Most people drastically underestimate the impact of a separation, so it’s important women plan ahead if they find themselves in that situation. Sadly, St Vincent de Paul found that older women are the fastest growing demographic of homeless in Australia - due to family breakdown or death of a partner. The costs of renting, especially in capital cities is a major issue resulting in homelessness for older women11.

Practical ways women can improve their financial lives in retirement

There are many things you can do now to improve your lifestyle in retirement:

-

If you’re leaving the workforce to care for children or a parent, discuss the financial impact with your partner or siblings and consider them contributing to your super. It’s worth noting, from 1 July 2017, it’s easier to claim the $540 tax offset for spouse super contributions

-

Try to contribute more to super while you’re still working. The earlier you start increasing your contributions the greater opportunity for your super to grow. Even small increased contributions make a difference - the returns you earn on your super can in turn earn returns the longer you’re invested. Remember, contributions to super, and earnings in super (below thresholds) are concessionally taxed

-

Become familiar with your retirement savings. Calculate what your super balance is likely to be at retirement and what that means in terms of how much you will be able to spend in retirement. Online calculators show you how you can improve your retirement income and are available on ASIC’s MoneySmart website.

-

Do a simple retirement budget. Many people over-estimate how much they will really need in retirement. See ASIC’s MoneySmart website for a range of super and retirement planning calculators

-

Look at all your assets, not just super. Make your money outside of super work hard for your retirement by investing it

-

Once you’re retired, stay invested. The investment earnings that you will make from 55 onwards, when your super balance is at its highest, will be a significant portion of your overall income in retirement

-

If you’re assessing potential employers, find out about their parental leave and super incentives

-

Speak to a financial adviser. It’s widely recognised that people who receive advice report better retirement outcomes and greater peace of mind12

-

And remember the government funded Age Pension currently covers basic spending needs for retirees that have low super balances subject to assets and income testing rules.

Key statistics - a visual summary

1. ‘Superannuation account balances by age and gender’, Association of Superannuation Funds of Australia, October 2017

2. Australian Bureau of Statistics, Gender Indicators, Australia, Catalogue no. 4125.0, Jan 2012

3. Australian Bureau of Statistics, Caring in the Community, Australia, Catalogue no. 4436.0 (2012), p 5.

4. Workplace gender equality agency, February 2017: ABS (2017), Labour Force, Australia, January 2017, cat. no. 6202.0

5. RICP Retirement Income Literacy Gender Differences Report, from The American College of Financial Services, July 2017’

6. ‘Financial literacy. Women understanding money’, Australian Government Financial Literacy Foundation 2008

7. Australian Bureau of Statistics, Life Tables, States, Territories and Australia, 2014-2016. Catalogue no. 3302.0.55.001

8. ‘Four ways men and women think differently when it comes to financial decisions’, NAB Asset Management, 2016

9. ‘ASFA Retirement Standard’, Association of Superannuation Funds of Australia – June quarter 2017

10. ‘The need to look deeper on the gender gap’, Willis Towers Watson, 2016

11. ‘Homelessness for older women – the hidden crisis’, St Vincent de Paul Society, Media Releases 2016

12. Rice Warner - www.ricewarner.com/valuing-financial-advice, September 2015

Source: MLC Hatch News & Insights June 6 2018

Important information

This information is provided by NULIS Nominees (Australia) Limited, ABN 80 008 515 633, AFSL 236465, a member of the National Australia Bank Limited (ABN 12 004 044 937, AFSL 230686) group of companies. An investment with NULIS does not represent a deposit or liability of, and is not guaranteed by, the NAB Group. The information in this communication may constitute general advice. It has been prepared without taking account of individual objectives, financial situation or needs and because of that you should, before acting on the advice, consider the appropriateness of the advice having regard to your personal objectives, financial situation and needs. NULIS believes that the information contained in this communication is correct and that any estimates, opinions, conclusions or recommendations are reasonably held or made as at the time of compilation. However, no warranty is made as to the accuracy or reliability of this information (which may change without notice). Past performance is not a reliable indicator of future performance. This information is current as June 2018 and may be subject to change, for example should there be a change of legislation or economic conditions.

Case studies in this publication are for illustration purposes only. Any general tax information provided in this publication is intended as a guide only and is based on our general understanding of taxation laws. It is not intended to be a substitute for specialised taxation advice or an assessment of your liabilities, obligations or claim entitlements that arise, or could arise, under taxation law, and we recommend you consult with a registered tax agent.